Swiss voters will soon head to the polls to decide on a reform that would introduce individual taxation for married couples. We took a closer look at the proposed bill – how would it change the tax system? Who would be the winners and losers? And more broadly, what sort of society do we want?

In a referendum on 8 March, Swiss voters will decide on a major change to the tax system: the introduction of separate rather than joint filing for married couples. Behind the technical jargon lies an age-old debate on how individuals should be taxed.

Under Switzerland’s current system, married couples are taxed jointly: their income and assets are added together and reported in a single tax return. For some couples this can lead to a higher tax burden than if they were not married (assuming the same level of income). People have criticized this aspect of the tax system for years, often referring to it as the “marriage penalty.”

Several past attempts at reform were largely unsuccessful. Like those efforts, the referendum on 8 March aims to dismantle the current system so that a person’s married status no longer directly affects how much tax they pay. But what’s at stake is more than just taxation. The proposed reform touches on broader issues such as the equal treatment of taxpayers, gender equality and the breakdown of paid labor within a couple.

The case for voting yes

For supporters of the reform, individual taxation would eliminate a form of tax discrimination. It would level the playing field between married and unmarried couples and could even encourage both spouses to work, which would be good news for gender equality.

The case for voting no

Those who oppose the reform believe it could create other forms of inequality, generate high administrative costs and disrupt cantonal tax systems that have already taken steps in this direction – without really solving the problem.

How would individual taxation work?

If the reform passes, each spouse would be taxed separately on their own income and wealth using the same rules as those for single people and unmarried couples. For now, the changes would apply only to the federal tax, although the idea is for cantons and municipalities to eventually adopt them too.

The reform also includes other targeted measures to address some of the costs that households bear. These measures include:

A higher deduction for children

The federal tax deduction for dependent children would be raised from CHF 6,800 to CHF 12,000 per child.

New tax rates

The tax rates for low- and middle-income individuals would be reduced so that the reform’s benefits extend to most tax brackets. The rate for high-income individuals would be increased slightly.

Implementation at all taxation levels

Individual taxation would eventually be implemented at not just the federal but also the cantonal and municipal levels. However, the exact rules would vary by canton since they have a considerable amount of legislative leeway. Because cantonal and municipal taxes account for most of an individual’s tax bill, it’s hard to gauge the extent – and particulars – of the reform for now.

Individual taxation in figures

We ran a number of simulations to determine who would be the winners and losers of the new system. We considered three different income levels and three different breakdowns of household income (by employment rate) within each couple.

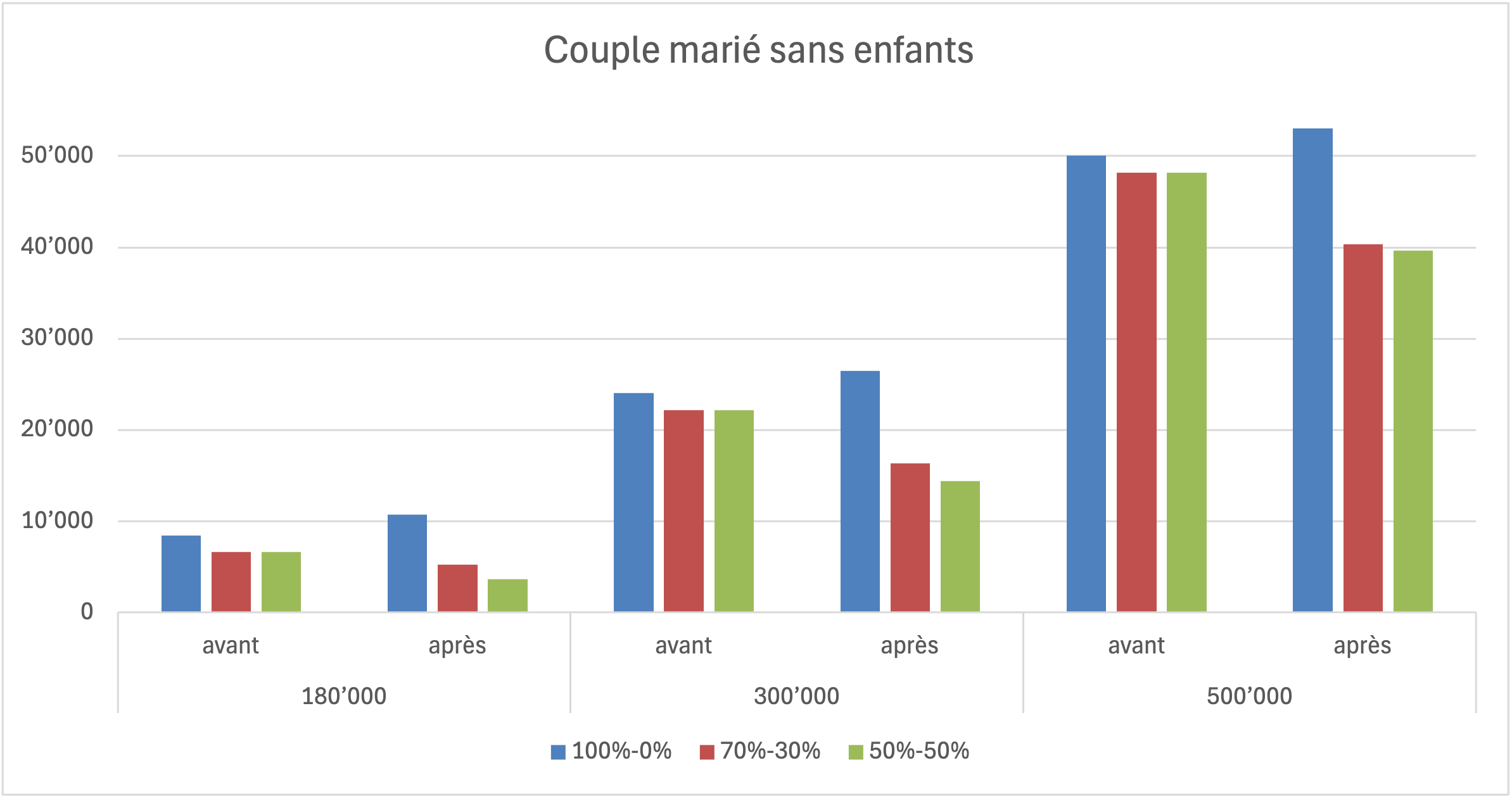

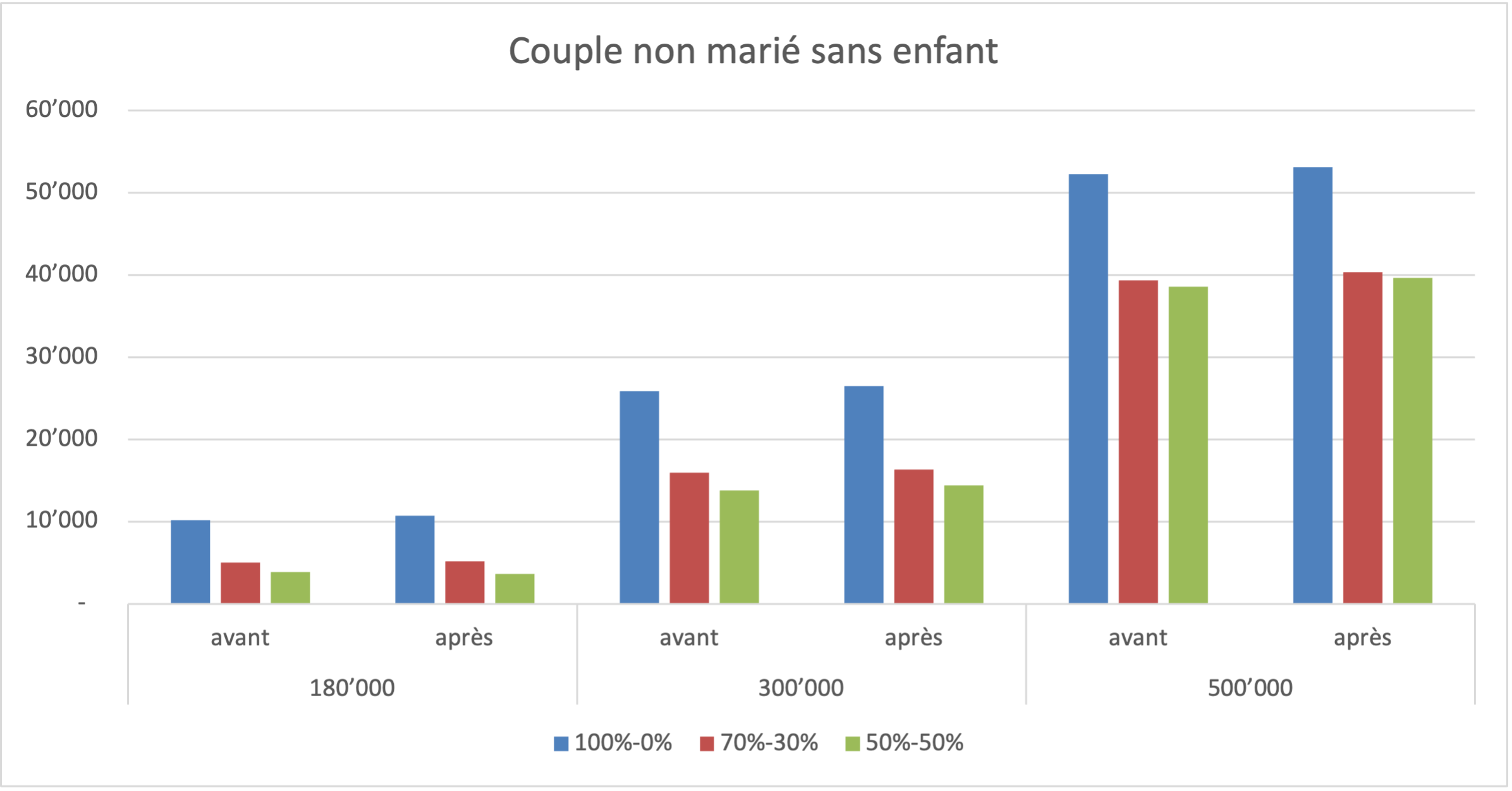

In the first simulation (two graphs below), we calculated the tax bill of a married and unmarried couple without children, before and after the reform.

The above graphs show that under the current system, there can be significant differences between the taxes paid by married and unmarried couples. Taking the example of a couple with a combined revenue of CHF 180,000 and a 50/50 split in household income, the federal tax bill would be CHF 3,811 if they are not married and CHF 6,602 if they are! But if the reform is passed, the tax burden would be CHF 3,646 in both cases.

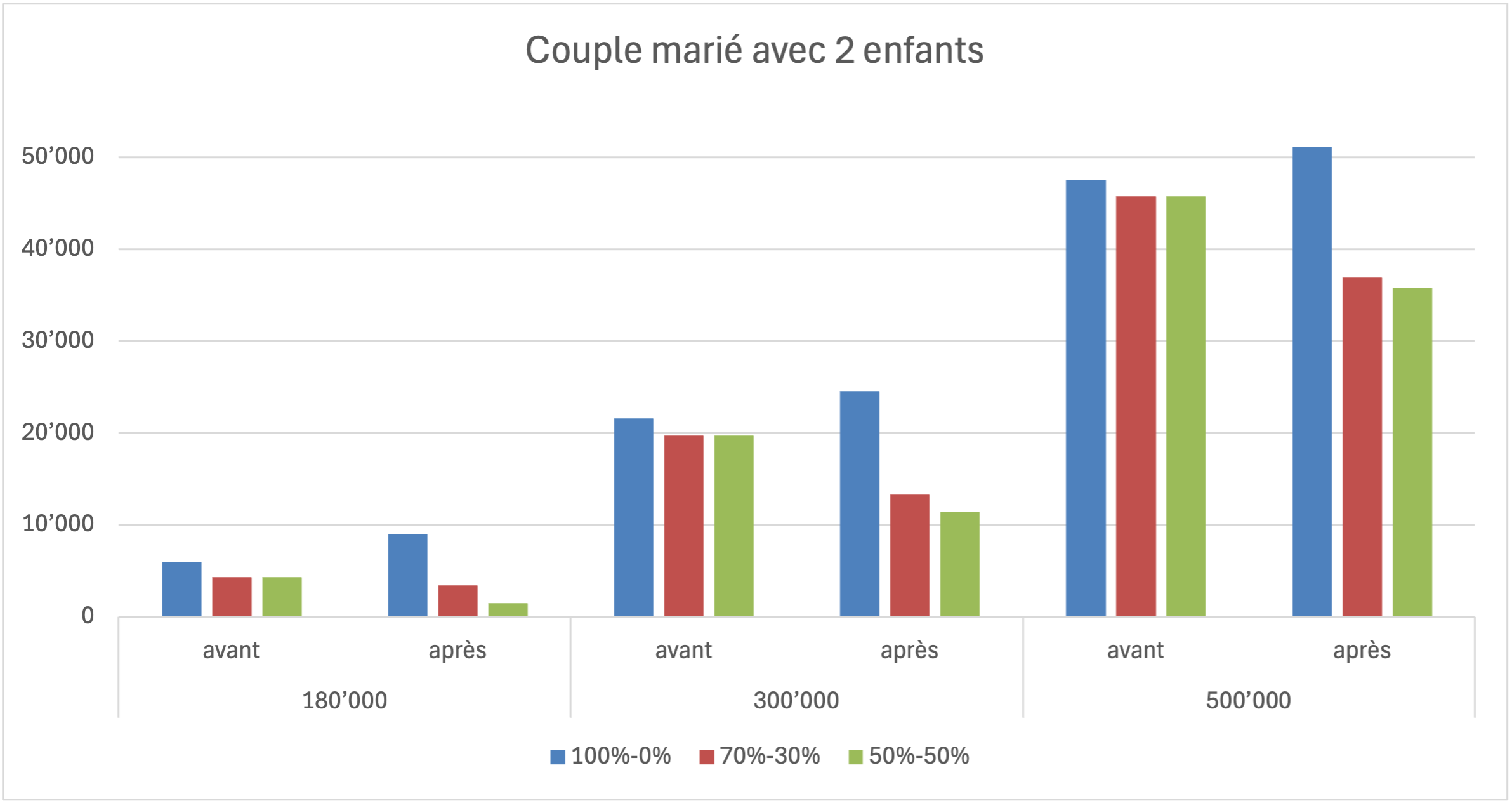

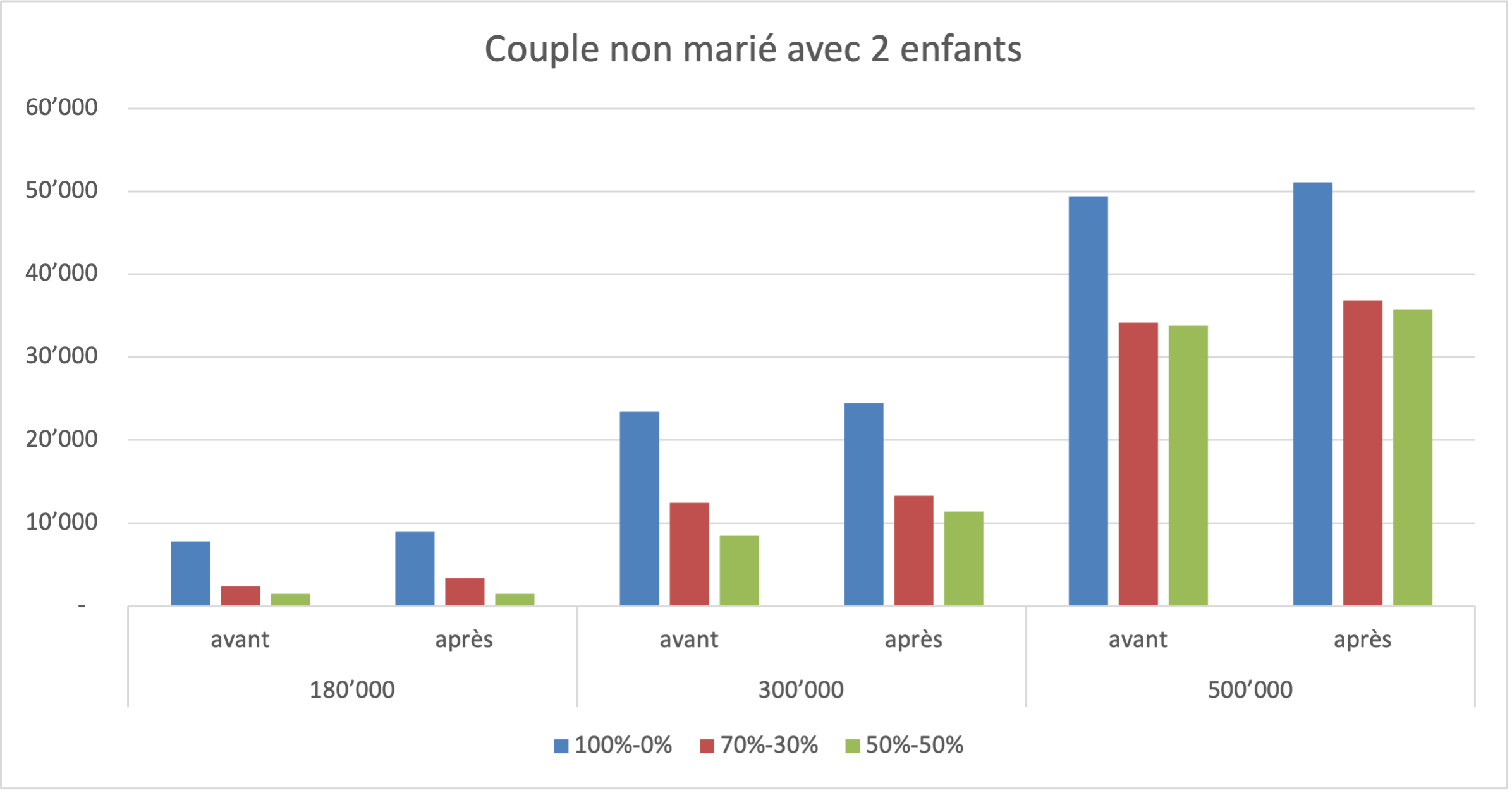

In the second simulation, we performed the same calculations but for a couple with two children.

These graphs show that the same pattern applies for married and unmarried couples with children. Although here, the reform could even be more beneficial for couples with children because the childcare deduction would go up.

Married couples in which both spouses work – regardless of whether they have children – would see the biggest drop in their tax bill, especially if they earn around the same amount. Low-income, unmarried couples in which the partners have similar earnings would also see their tax bill decline owing to a lower tax rate.

The changes provided for in the reform seem fair, but they would naturally come at a cost. Doing away with the “marriage penalty” would reduce the federal government’s tax intake by an estimated CHF 630 million.

At this point we can’t estimate what the impact would be for cantons and municipalities because a lot depends on how the reform is implemented at those levels.

A choice with ramifications for society

The consequences of introducing individual taxation for married couples need to be assessed on a case-by-case basis. The reform wouldn’t be a disaster or a jackpot for everyone. Some households would win, some would lose and most would see very little change. But when deciding how to cast their vote, Swiss citizens also need to think about what the reform would mean for society.

The new system would encourage both spouses to contribute as equally as possible to household income. It would also allow for higher childcare deductions. Those are good incentives. Today, many women with children hesitate to go back to work, in part because their salary would be almost entirely eaten up by taxes and childcare costs. So in that sense, individual taxation would be a positive step.

Looking further out, the reform could even encourage part-time work, especially by men. It would be more tax advantageous for a couple if both partners work at 80% than if one works at 100% and the other at 50%. This could enable greater career fulfillment and lead to better gender equality within a couple.

For all these reasons, switching to individual taxation would seem to be a constructive, modern choice. It would also eliminate what is increasingly becoming an outlier vis-à-vis the rest of the world: most countries today tax spouses individually, although some offer the option of filing jointly or have made certain adjustments to account for family circumstances.

More granular tax planning

The new system would necessarily be more complicated, as each couple’s specific circumstances would need to be taken into account. It would clearly create additional challenges for our tax planning and optimization business. For instance, we’d be less able to rely on the low hanging fruit, such as suggesting that couples make alternating voluntary contributions to their retirement accounts.

We would therefore take an even more granular view and dig into the details, including on issues related to timing. And we could find ourselves making completely novel recommendations, like suggesting one spouse increase their employment rate while the other decrease theirs.

As always, don’t wait until the last minute – contact us today so we can help you plan for the future as efficiently as possible.